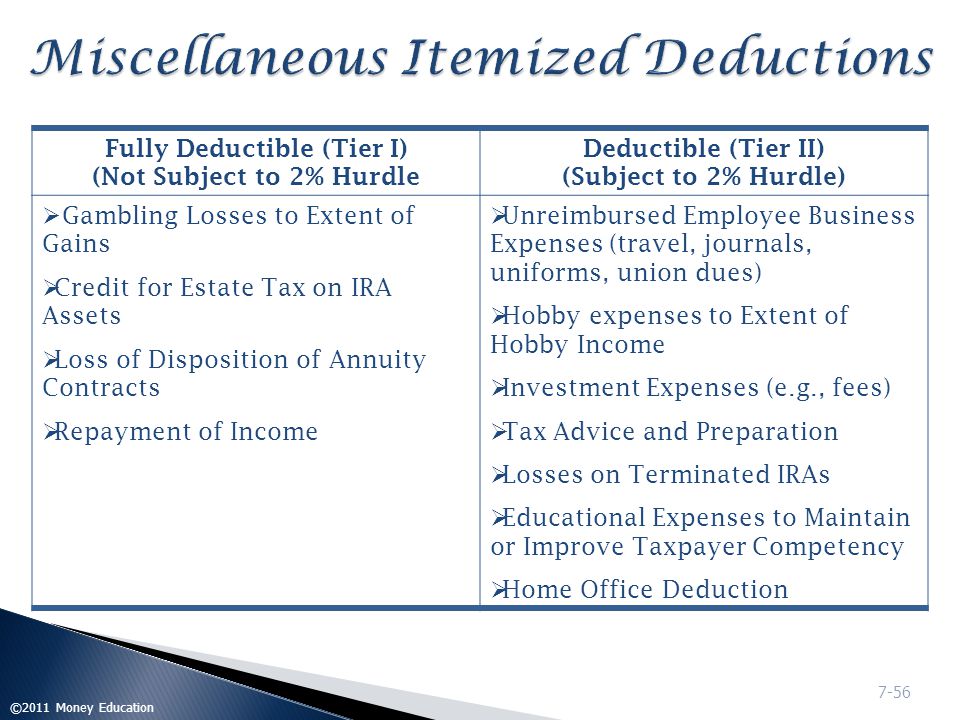

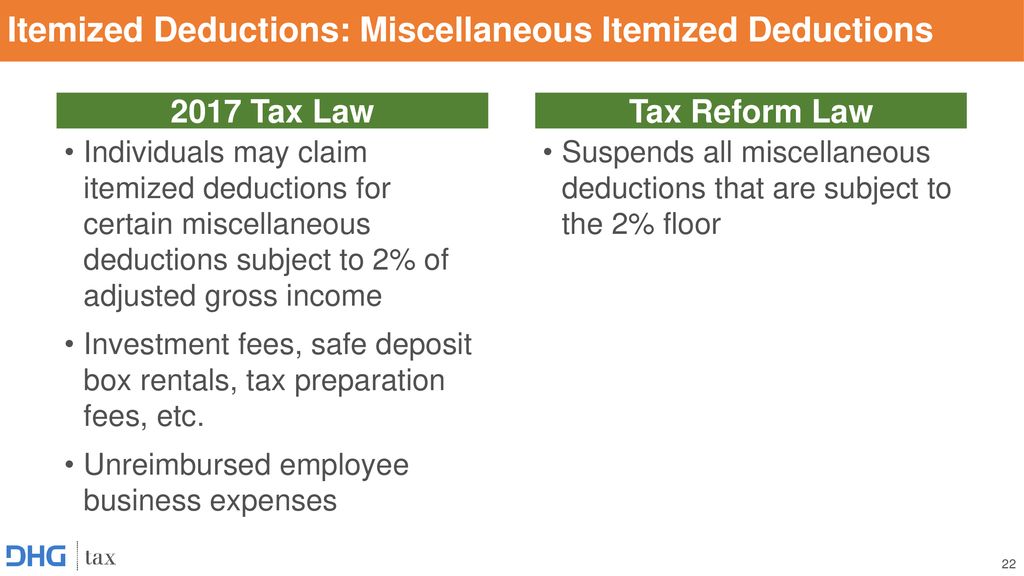

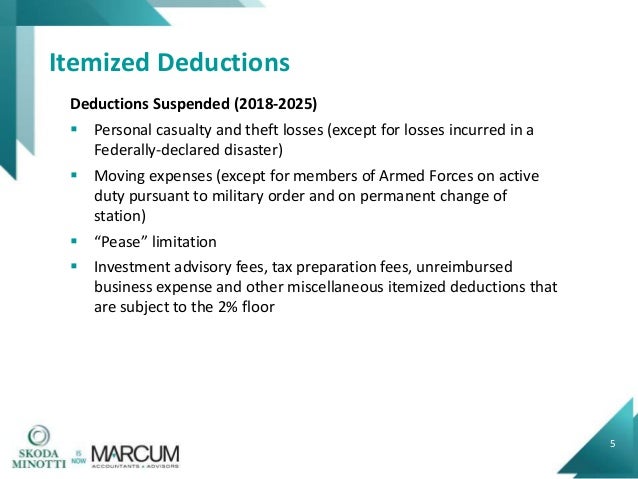

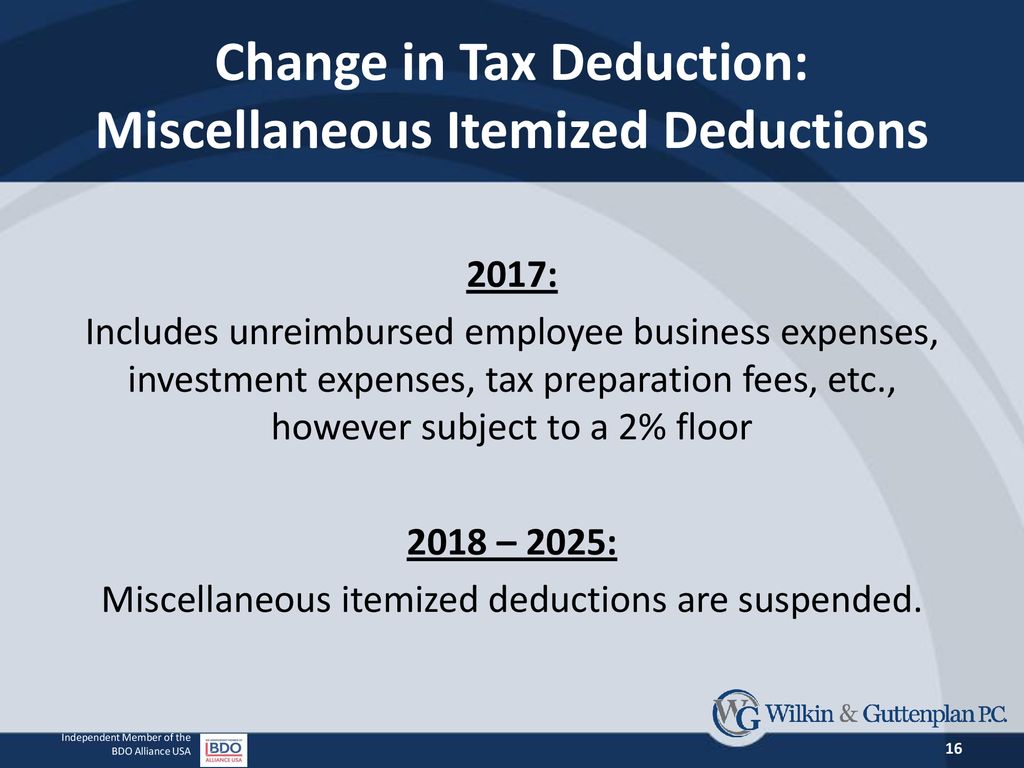

Miscellaneous Itemized Deduction Subject To A Two Percent Floor

Tax Reform 2018 The Impact On Itemized Deductions For Individuals Jfs Wealth Advisors

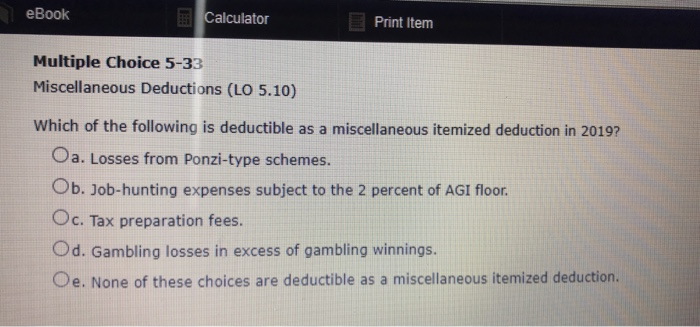

Solved Ebook Calculator Print Item Multiple Choice 5 33 M Chegg Com

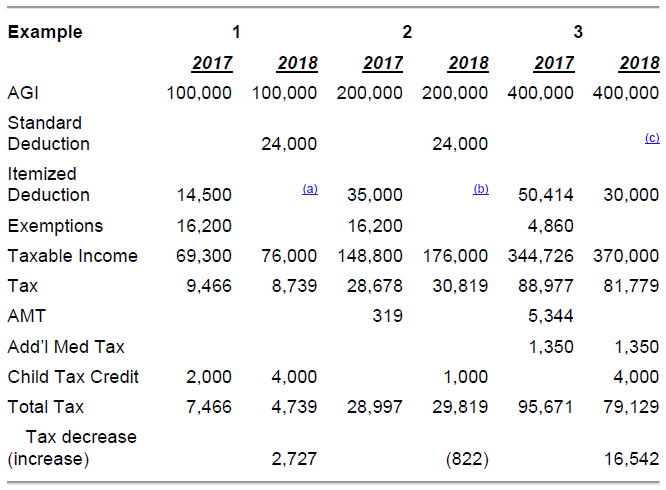

Acct321 Chapter 06

Vol 01 Chapter 10 2015

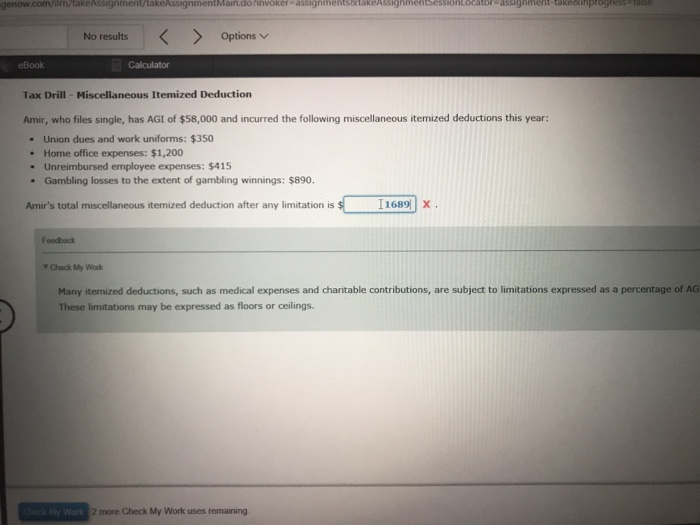

Solved I Need To Know How To Do This So Please Explain Yo Chegg Com

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

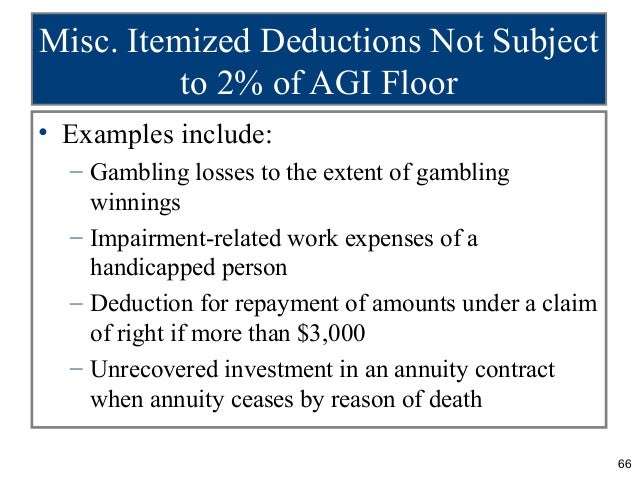

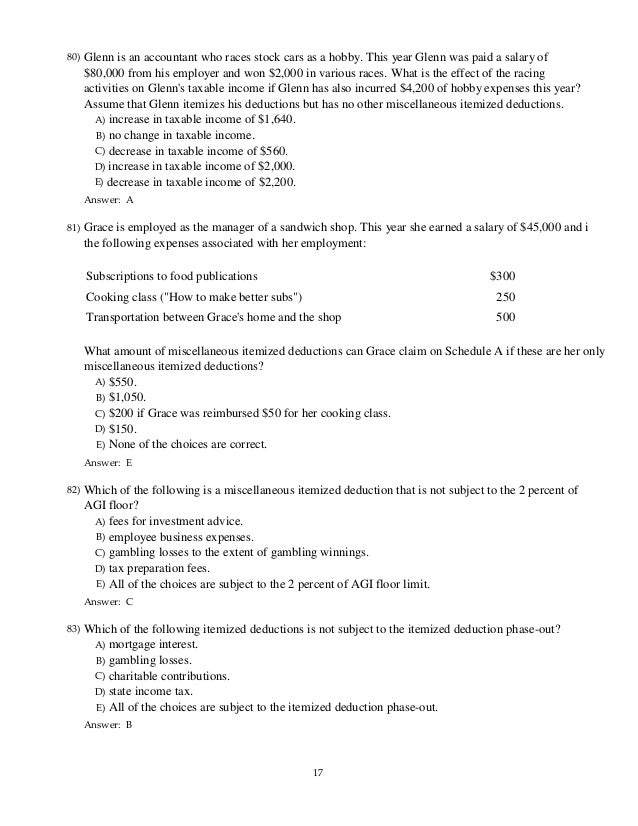

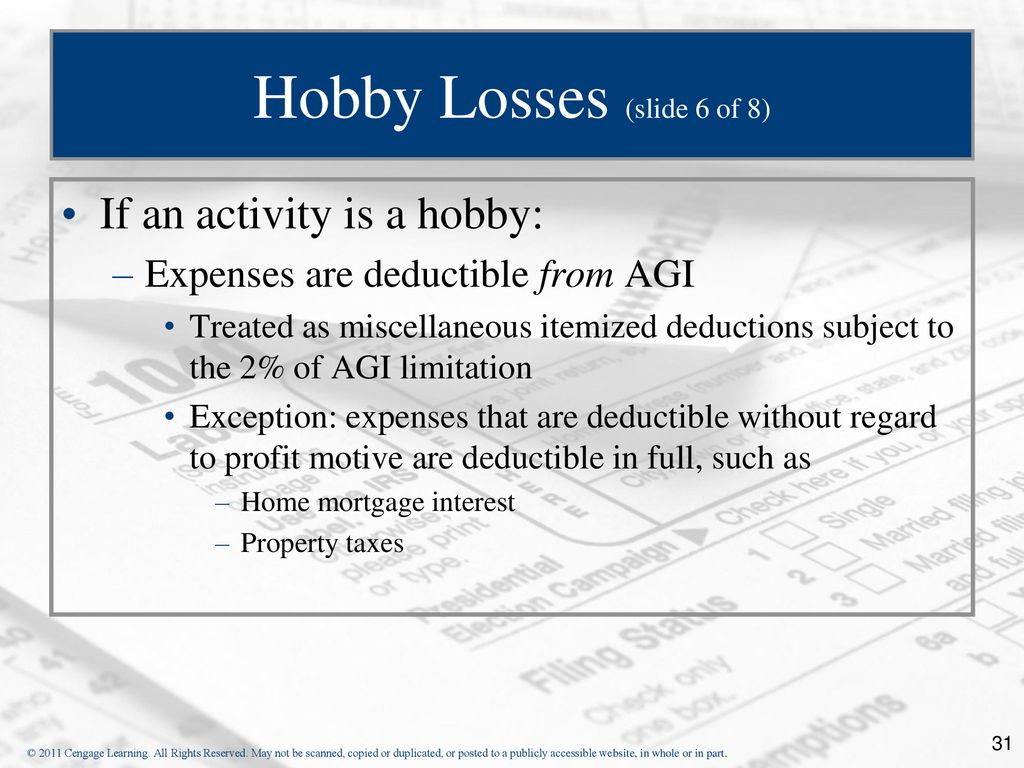

A type of expenses subject to the floor 1 in general.

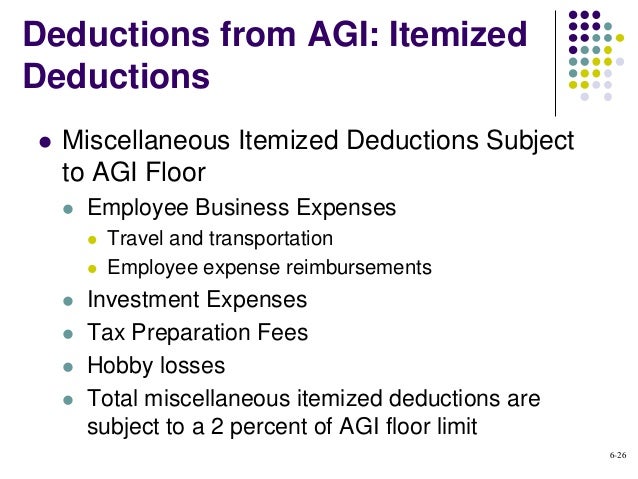

Miscellaneous itemized deduction subject to a two percent floor.

Itemized Deductions Chapter 7 C 2009 Money Education Ppt Download

Cfp Income Tax Planning Flashcards Quizlet

Webinar Slides Tax Reform S Impact On High Net Worth Individuals

2017 Tax Cuts Jobs Act Impact On Families

Acct 421 Chapter 9 Flashcards Quizlet

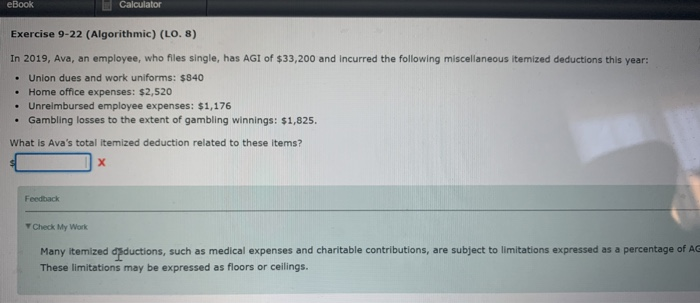

Solved Ebook Calculator Exercise 9 22 Algorithmic Lo Chegg Com

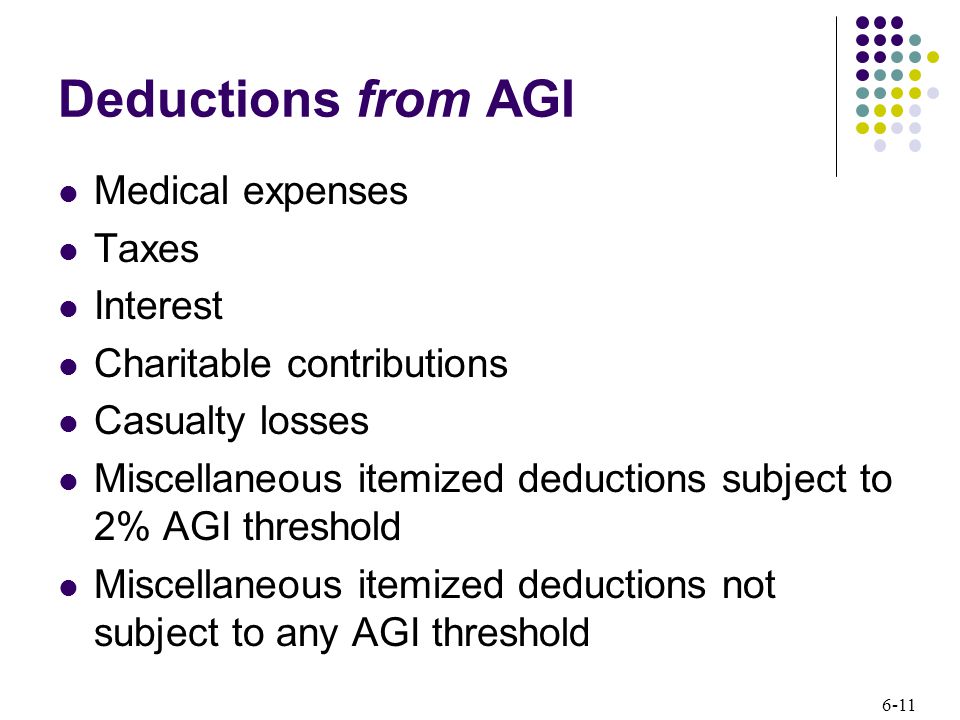

Mcgraw Hill Irwin Copyright C 2012 By The Mcgraw Hill Companies Inc All Rights Reserved Chapter 06 Individual Deductions Ppt Download

Acc 547 Final Exam Answers 2015 Version

Highlights Of The Tax Cuts Jobs Act Ppt Download

Deductions And Losses In General Ppt Download

The Life Of The Bill June 2016 September 27 2017 November 16 Ppt Download

Navigating Tomorrow S Tax Landscape 2020

Investment Fees Are Not Deductible But Borrow Fees Are Investing Best Term Life Insurance Life Insurance Companies

Hunterdon Somerset Association Of Realtors Taxes For Realtors Ppt Download

Http Www Ipbtax Com Assets Htmldocuments Aba 20chang 20170 1 V2 Pdf

Middle Class Tax Deduction Act Of 2019 H R 1867 Govtrack Us

Top Five Tcja Tax Planning Opportunities For Individuals In 2018 Lehigh Valley Elder Law Law Offices Vasiliadis Pappas

Irs Clarifies Estate And Trust Expense Deductions Mcb Tax Advisors

Chapter 14 Taxes Federalsoup Com

Internal Revenue Bulletin 2020 22 Internal Revenue Service

The Tax Cut Impacts Investors In Negative And Positive Ways Greentradertax

Miscellaneous Itemized Deductions For Tax Year 2018 Montana Department Of Revenue

Acc 455 Effective Communication Uopcourse Com

2019 Tax Filing Season 2018 Tax Year Itemized Deductions Everycrsreport Com

Family Office Investments And Business Interest Proposed Regulations Tax Executive

Trusts Msk Blog

A Closer Look At Miscellaneous Itemized Deductions

Instructions For Form 2106 2019 Internal Revenue Service

0if4quio4fujem

Irs Clarifies Estate And Non Grantor Trust Expenses Not Subject To Miscellaneous Itemized Deduction Suspension Notice 2018 61 Tax Accounting Blog

What Is The Standard Deduction Vs Itemized Deduction H R Block

Tax Deductions For Individuals A Summary Everycrsreport Com

Proposed Regulations Upon Which Taxpayers May Rely Issued For Excess Deductions On Termination Current Federal Tax Developments

10 Ways Tax Reform Is Impacting Financial Services Ksm Blog Katz Sapper Miller Cpa

Significant Itemized Deduction Changes For 2018 Berntson Porter Company Pllc

A List Of Eliminated Tax Deductions For 2018 Returns Taxact Blog

When Is Interest Expense Deductible Taxact Blog

Gale Academic Onefile Document High Income Tax Returns For 2012

The Long Lasting Impact Of Tax Reform Long Island

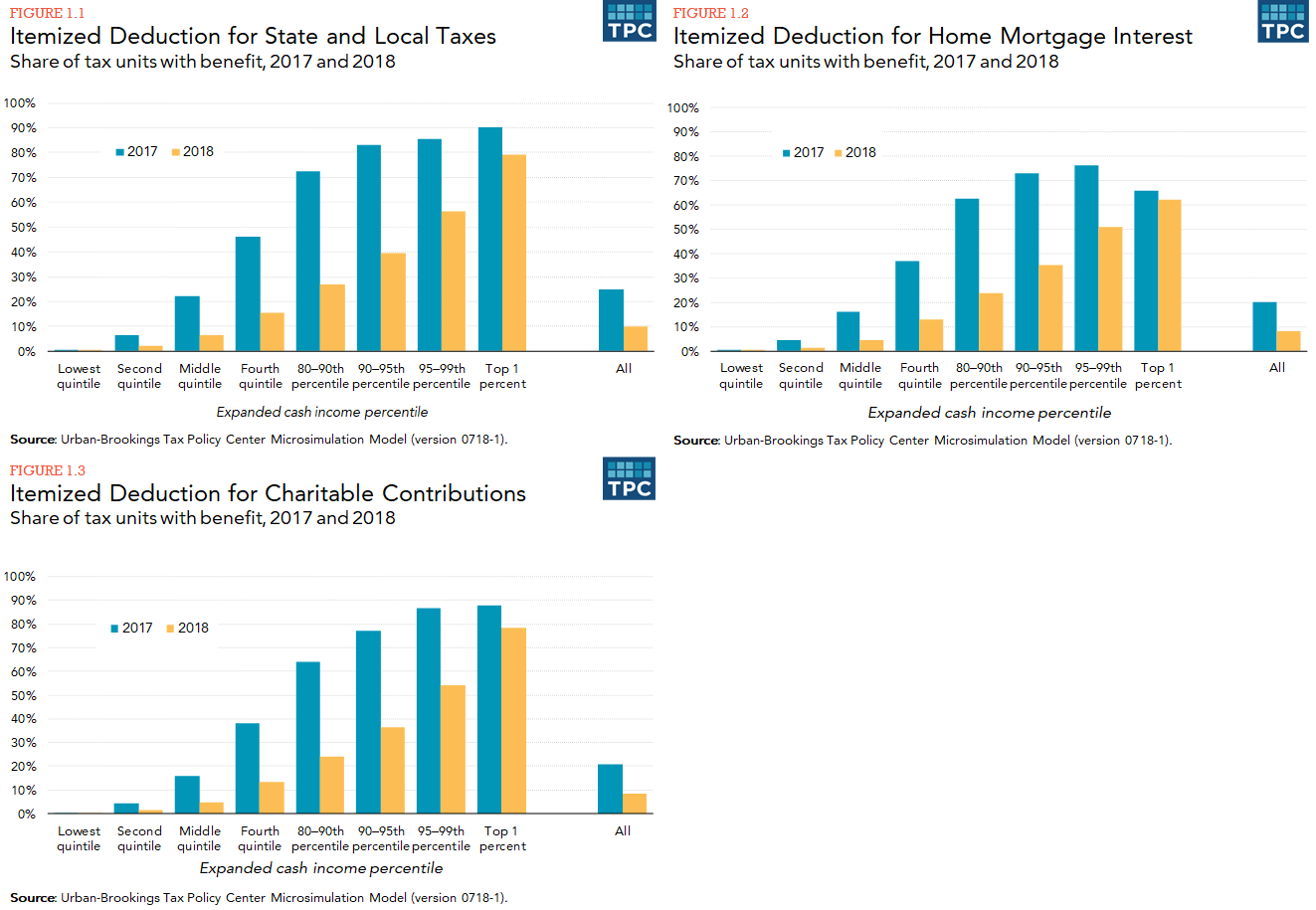

How Did The Tcja Change The Standard Deduction And Itemized Deductions Tax Policy Center

Miscellaneous Tax Deductions To Claim On Your Tax Return

Gale Academic Onefile Document Individual Income Tax Returns 2001

Chapter 5 Itemized Deductions Other Incentives Ppt Download

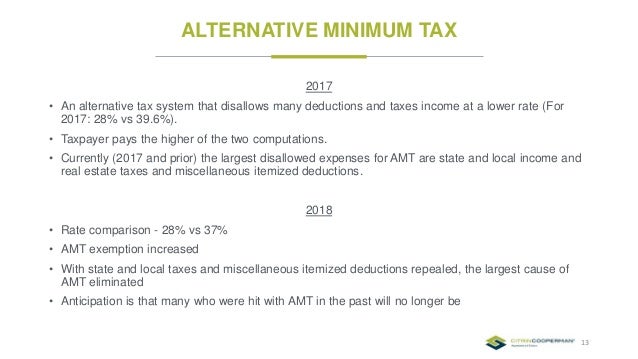

Individual Alternative Minimum Tax Planning And Strategies Ppt Download

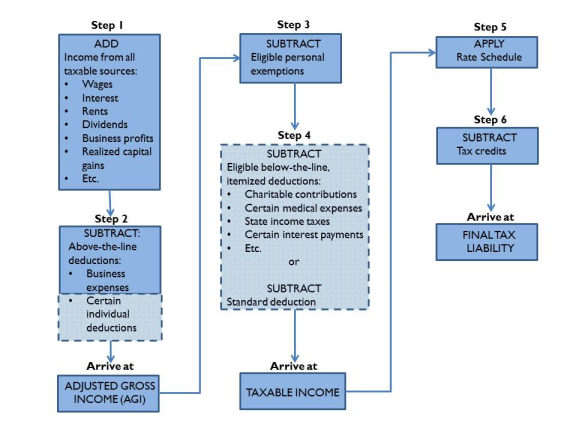

Source : pinterest.com